The breakthrough year of 2025 has set the stage for what promises to be fleet management's most pivotal period yet. AI-powered fleet management moved from experimentation to operational reality, driving measurable improvements in route optimization, predictive maintenance, and operational excellence. Now, as we stand at the threshold of 2026, the industry faces a fundamentally different challenge: the separation of leaders from laggards will be determined by the ability to integrate AI as an operational partner and transform high-quality data into competitive advantage.

In 2025, AI-powered fleet management transformed fleet operations all over the world, electric vehicle sales crossed the 20% global market share threshold (although with striking regional variations), and autonomous vehicles expanded their commercial footprint. Last-mile operators are pioneering bold multimodal approaches that seamlessly blend traditional motorized fleets with cargo-bikes, on-foot delivery, sidewalk robots, and even early aerial delivery experiments.

Fleets need to focus on building a cohesive operational strategy that delivers lower costs, higher efficiency, and competitive advantage in an increasingly complex and technological mobility landscape.

The rise of the AI-powered fleet

2025 saw optimized, AI-empowered fleet management moving decisively from pilot projects to an industry standard, driven by the tangible benefits realized at scale.

Numerous fleet operators around the world optimize operations using advanced data ingestion and workflow automation to handle critical fleet operations, including dynamically adding and removing vehicles from the active inventory based on their current state, implementing maintenance triggers, and orchestrating charging for electric vehicles.

This shift has been accelerated by the need for greater efficiency, cost reduction, and the competitive advantage conferred by minimizing vehicle downtime. Real-world deployments have reported up to a 71% reduction in downtime and 25% fewer tasks. However, a recent Gartner study has shown that the benefits of AI are not equally felt across the organization (regardless of industry). Fleets should employ smart change management strategies, involving multiple stakeholders, if they are to maximize the benefits of this AI revolution.

AV continues to expand

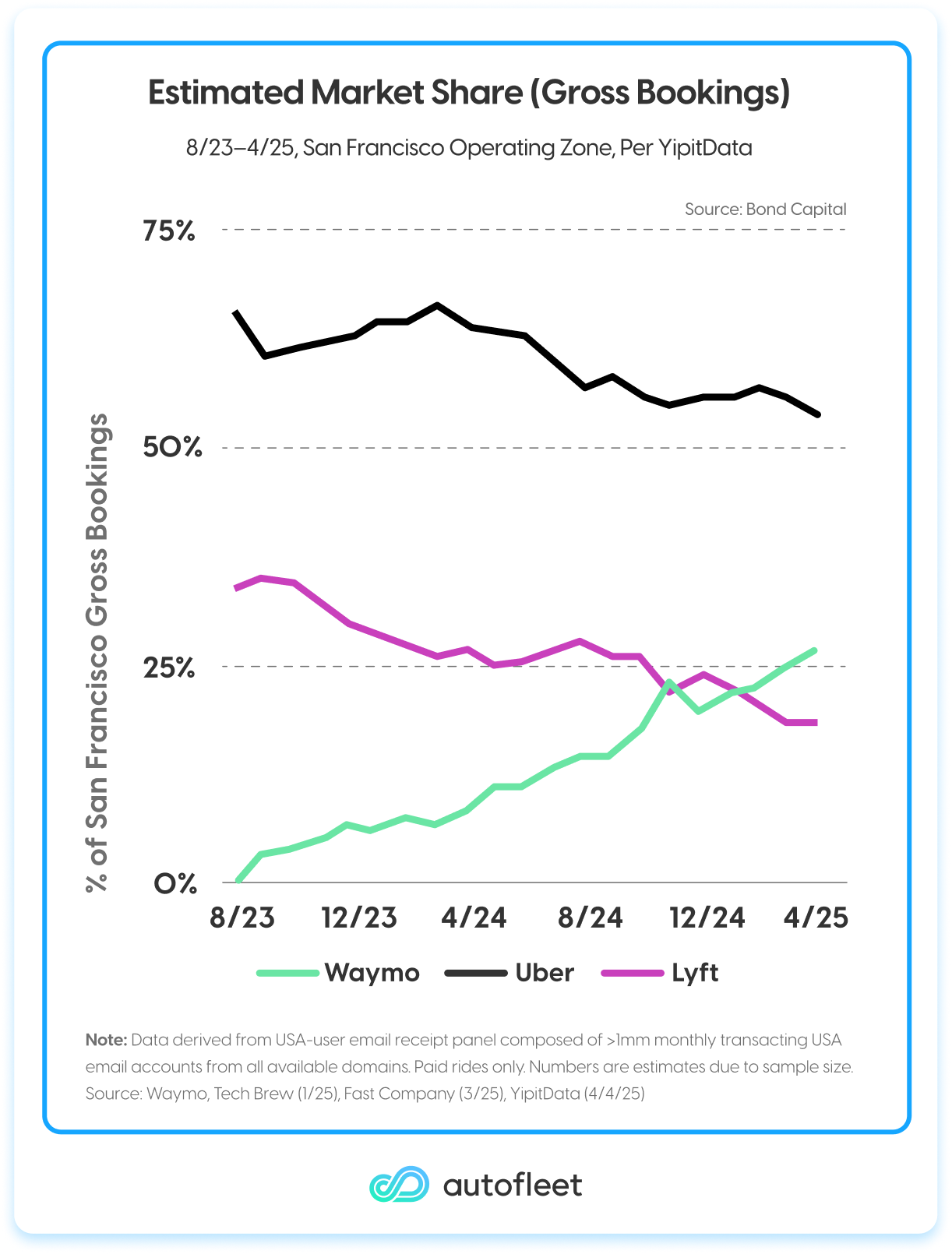

Nowhere is the impact of AI more apparent than in Autonomous Vehicles (AVs), which are physical AI-in-motion robots. As of late 2025, autonomous vehicles continue their persistent growth, with commercial deployments, mostly in urban areas in the US and China, and planned expansions worldwide.

Privately owned vehicles with some autonomous capabilities (typically level 3 that still require the driver's full attention) are getting more common, leading Elon Musk to suggest Tesla owners will be able to text and drive soon. However, the action is banned nearly everywhere.

But Robotaxis using full self-driving, Level 4, vehicles are a common sight in cities like San Francisco and Phoenix, and they are becoming more diverse as more and more manufacturers enter the field. Looking ahead to 2026, we expect strong continuous growth as the global autonomous vehicle market is projected to grow over tenfold by 2035, with broader use in logistics and public transport likely in regions like Europe.

One element holding AV deployment back is the lack of regulatory clarity. Despite data showing AVs to be safer than human drivers, AV deployment still relies on limited local initiatives to allow self-driving cars onto roads. This is being addressed both in the US and on a global level by the UN, which is working on a new set of regulations expected by mid-2026, and which will be critical for wider adoption.

Another challenge facing autonomous vehicles today is the complexity of managing an entire fleet of these vehicles at scale. Unlike traditional fleets, AV fleets require sophisticated systems for real-time monitoring, predictive maintenance, incident response, and remote supervision to ensure safety and operational efficiency. Optimizing fleet operations, reducing downtime, and handling safety-critical events in real time are central to successful AV deployment.

Mobility-as-a-Service and Embedded Mobility

The expansion of AV solutions, alongside the growing need to meet more transportation requirements with less budget, has given rise to a resurgence of interest in the potential of Mobility-as-a-Service and Vehicle-as-a-Service approaches that incorporate autonomy alongside shared vehicles.

This is coupled with a newer concept of Embedded Mobility, i.e., the integration of transportation and mobility services directly into the ecosystem. Making mobility access seamless and contextual rather than requiring users to seek out separate transportation services, and providing contextual access to various transportation options.

The jury is still out on how this will play out. Will transportation become completely commoditized? Will economies of scale and access to data create monopolies? We suggest remaining watchful in 2026 to see where the market is heading.

EV adoption accelerated globally, with large regional variations

As we predicted last year, the IEA's Global EV Outlook 2025 confirmed that electric car sales surpassed 20% global market share. This is also driven by energy costs volatility that some expect will continue to plague 2026. Industry data also confirms that EV maintenance costs run approximately 30% lower than ICE vehicles.

But the market is showing a lot of regional variation. In China, EVs are projected to reach 51.6% of light-vehicle sales in 2025 and 73% by 2030, driven by competitive pricing and government support. In Europe, plug-in vehicles rose to 28% despite macroeconomic headwinds, thanks to new incentives and stricter CO₂ targets, but growth is slowing.

Meanwhile, in North America and Australia, despite a rush in Q3 to get the now-expired incentives for EVs, EVs are slowing, and some are even predicting negative growth. On the other hand, hybrid electric vehicles continue to gain market share, possibly indicating a happy medium that may accompany these markets for a while before they embrace EV in full. US tariffs and EU duties also impact China-made BEVs, affecting pricing and availability.

Fleet composition and vehicle prices

According to Element Fleet Management's insights, the top vehicles acquired by fleets in 2025 demonstrated a varied mix of powertrains.

Internal Combustion Engine (ICE) vehicles remained prominent, with the Subaru Forester, Ford F-150, Chevrolet Silverado 1500, and Chevrolet Equinox leading sales.

Hybrid models saw accelerating adoption, marked by significant demand for the Ford Maverick, Toyota Camry, Toyota RAV4, Ford Escape, and Ford F-150 Hybrid. Within the electric vehicle (EV) segment, the Mustang Mach-E and F-150 Lightning were key drivers of fleet adoption. Despite Ford’s F-150 relative popularity, it has announced it is pausing production of the pure EV model, since its electric vehicle unit has continued to post losses and U.S. demand for electric trucks is still limited.

When examining Total Cost of Ownership (TCO), residual value analysis reveals that the Toyota Corolla continues to lead among ICE vehicles, while the Hyundai Kona performs best in the EV segment.

Maintenance cost analysis shows notable advantages for specific models, with EVs like the GMC Hummer and Rivian R1T, and ICE vehicles including the Toyota Crown, Hyundai Santa Fe, and Mazda 3 demonstrating the lowest maintenance expenses. and ICE resale values as a percentage of capitalized cost have held up more strongly than EVs over the evaluation period

Telematics data is consolidated and becomes actionable

The fleet management industry is veering towards open software platforms that unify and aggregate both OEM-embedded and aftermarket telematics data into a single control plane with live KPIs and closed-loop actions.

This "Super App" approach not only eliminates the chronic "app fatigue" that has plagued fleet managers who previously had to juggle separate systems but also allows businesses to bridge the gap between operational and telematic data, enhancing the fleet’s capabilities across the board. Unifying data into a single source of truth also enables the implementation of AI-driven analytics that move beyond reactive dashboards to proactive, prescriptive actions.

New tools like advanced in-cabin camera systems and natural language interfaces (like Autofleet’s Nova) are becoming increasingly popular. Data is used beyond just staring at dashboards, democratizing fleet insights through conversational analytics, providing comprehensive visibility into driver behavior, safety events, and operational compliance, and more.

This consolidation trend also helps fleets meet intensifying regulatory requirements, particularly in Europe, where the Corporate Sustainability Reporting Directive (CSRD) is in place (despite some recent simplification and timeline adjustments), making telematics-derived data an essential component of fleet management.

Last-mile delivery leading innovations in multimodality and the aerial medium

Last-mile delivery is emerging as a catalyst for breakthrough innovations in multimodal logistics and aerial transportation as we move through 2026. The sector is witnessing unprecedented integration of multiple transport modes, including traditional vans, autonomous delivery bots, bicycles and cargo-bikes, and even walking. Some last-mile delivery companies and retailers (notably Amazon and Walmart) also started experimenting with aerial delivery through drones.

This multimodal approach may be a natural extension of the logic guiding logistics companies that leverage each transport mode's strengths throughout the journey, using rail and maritime for cost-efficient bulk transport, or airplanes for speed, for example.

This gives rise to new route planning challenges, requiring optimization across multiple transportation modes, and the creation of complex routes that combine multiple transport modes - such as driving, parking, and walking.

Looking ahead into 2026 and beyond

For me personally, 2025 marks the launch of Element Mobility, the strategic division dedicated to driving the future of intelligent fleet technology by bringing together breakthrough technologies, forward thinking, and transformative partnerships. We are taking a proactive stance in shaping the industry as it is goes through transformative changes, particularly the rise of AI, AVs, and intelligent fleet technologies.

In 2026, we enter a decisive phase where the fleet and mobility industry integrate technology into its operations. AI is transforming fleet intelligence, enabling dynamic optimizations and automated decision-making across entire operations. Autonomous vehicle deployment is scaling and requires a shift in perspective: from a single vehicle going from A to B, to fleet operations.

Fleets will be judged on their ability to execute the new capabilities offered by technological advancements. Success will hinge on building strategic partnerships, robust data infrastructure, and scalable operational frameworks. Organizations that master this integration will be able to extract the maximum value from their fleets.

Table of сontents